By Dr Charles Ellinas, @CharlesEllinas

Councilor, Atlantic Council

In the present climate, with the world transiting to clean energy and net-zero emissions by 2050, the long-term future of natural gas is not assured. Even though it will continue to be an important component of the energy mix during transition, demand for it is likely to peak during the 2030s and decline thereafter.

In 10-15 years from now the world may be facing more challenging gas markets – as Europe is now. If plans to export East Med gas outside the region do not mature soon, it risks missing the export-boat altogether.

It is necessary to understand these evolving forces that are shaping energy globally if we are to understand the energy security dynamics around the East Med.

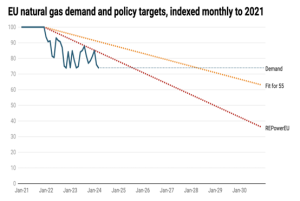

Replacement of Russian pipeline gas to Europe has largely happened. Longer-term Europe’s REPowerEU policy is to reduce reliance on natural gas – by 52% by 2030 and more or less completely by 2050. So far gas consumption in Europe has declined close to 25% in comparison to the 2017-2021 average (Figure 1). But there are growing markets for gas in Asia, should export become possible through new gas discoveries around the East Med.

Figure 1: EU natural gas demand and policy targets

Source: Bruegel

The future is regional

Currently known gas reserves in the East Med are not sufficient to support major new export-orientated projects. Fortunately, we have a massive market in the region that can absorb all this gas: Egypt. In the longer-term, and depending on geopolitical developments, this could also include Turkey.

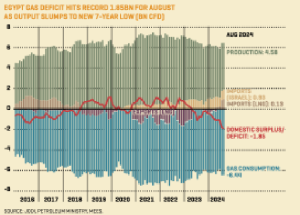

Years of declining production have turned Egypt from an exporter to an importer of LNG to satisfy its ever-growing demand for gas for power generation (Figure 2), but also as feedstock for its petrochemical and fertiliser industries.

Figure 2: Egypt’s natural gas deficit

Source: MEES

But this is an expensive option that cannot be supported in the longer-term. In 2025 alone, the country is expected to spend about $8billion on LNG imports, that could have a crippling effect on its beleaguered economy.

Securing sufficient gas supplies to avoid blackouts is also critical to the country’s political stability, a factor that weighs heavily in the minds of its neighbours.

Egypt has already turned to Israel, where new projects have been sanctioned to increase gas exports to Egypt from about 10bcm/yr now to 21bcm/yr by 2028.

The country is also in discussions with Cyprus to import gas from the 2.5tcf Cronos and 3.5tcf Aphrodite gasfields, with inter-governmental agreements to facilitate these projects already signed. These have cleared the way for the field operators, Eni and Chevron, to agree field development plans with Cyprus ministry of energy.

The big challenge, though, that weighs heavily in the minds of the oil and gas companies, is Egypt’s ability to maintain regular payments in the longer-term and willingness to pay market-prices for this gas. These are the main reasons why, so far, these companies have not been expediting new gas projects in the country.

The ExxonMobil factor

Following successful exploratory drilling in Egypt’s North Marakia block, ExxonMobil has just started drilling a promising target, Electra, in Cyprus block 5, to be followed by Pegasus in block 10.

Should Electra turn-out to be as big as some reports claim, 30tcf, it would require a number of appraisal wells over 2-3 years before development options can be firmed-up. Depending on the shape of the global LNG market in the next decade, discovery of even 10tcf or more gas could be sufficient to support a world-class LNG export project, targeting Asia. The most-likely location of such a project could be Vasilikos in Cyprus, but another option would be the now-unutilized LNG plants at Idku and Damietta in Egypt, with a combined capacity of 12,5million tonnes LNG per year.

But given ExxonMobil’s processes for planning and sanctioning new major projects, such a project is unlikely to become operational before the early 2030s.

Other developments

Cyprus electricity system is isolated and in need of a major overhaul. In order to expedite the development of its renewables sector, Cyprus is pursuing electrical inter-connection with Crete and through there to Greece and Europe. The Greek Independent Power Transmission Operator is in the process of constructing the €2bn HVDC Great Sea Interconnector, about 1200km long.

Perceived geopolitical risks associated with Turkey’s maritime claims in the region appear to be manageable and not expected to stop progress.

Completion of this project, expected by 2030, will lift this isolation and facilitate the further expansion of renewables on the island.

Conclusion

Clearly it is important to develop energy resources and utilize as much as possible regionally to cover the region’s growing energy needs during transition. Today gas and LNG can contribute to decarbonisation by displacing oil and coal in the power sector.

To that extent, regional cooperation to facilitate exploitation of East Med’s natural gas resources can make a difference.